Your Pension is a Big Deal. Here’s Why.

Let’s be honest: pensions aren’t the most exciting topic. But if you’re a member of HSA, your pension might be one of the most valuable benefits you’ll ever earn.

Most HSA members are part of the Municipal Pension Plan (MPP), which is a defined benefit (DB) plan. If you’ve heard that term and not sure what it means, you’re not alone. But understanding your DB pension plan could change how you plan for your future.

What is a Defined Benefit Pension?

A DB plan, like the MPP offered to HSA members, is a promise. A promise that when you retire, you’ll receive a predictable, guaranteed monthly income based on your salary history and how long you’ve worked. The “pension promise” is an essential feature of a DB plan.

This type of plan is attractive because it offers financial security and stability. It removes the uncertainty regarding how much money a worker will have in retirement. It means that you can plan your future with confidence, knowing that every year you work is building towards a secure retirement. You won’t have to guess what you’ll have when you stop working. You’ll know.

That kind of peace of mind is rare.

While critics sometimes claim defined benefit plans are too generous or unsustainable, these charges often confuse public-sector DB plans like the MPP with single-employer corporate plans. These types of plans are quite rare in 2025. In addition, many of these criticisms are based on historical problems with single-employer plans, and pension legislation has evolved to address these issues.

In truth, Canada has a public sector pension model, jointly trusteed by employers and unions, that is internationally recognized as a top example of success in retirement security. It’s strong, sustainable, and jointly managed.

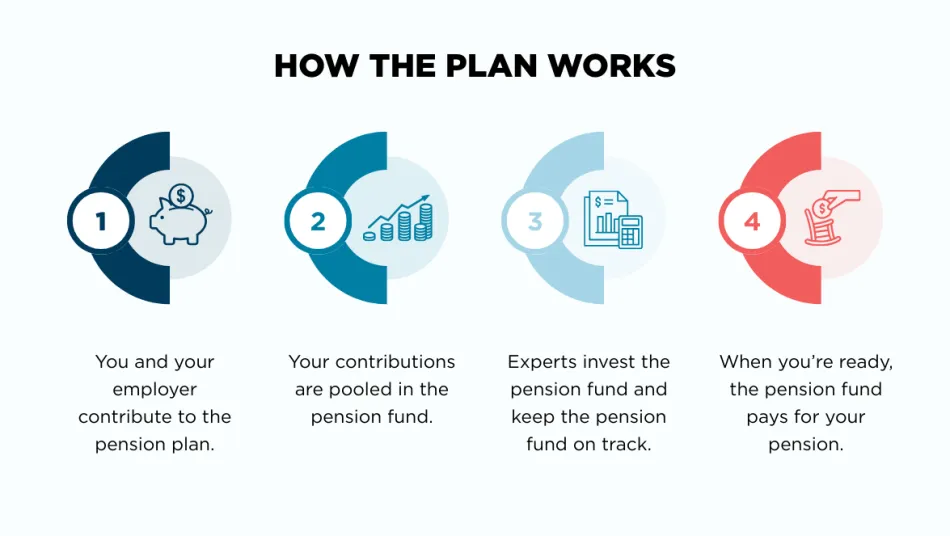

The MPP is one such multi-employer jointly trusteed plan. That means that representatives of both union members and employers bear the responsibility for administering the plan and managing the investments, ultimately ensuring that employees receive their promised benefits upon retirement.

The MPP is fully funded and carefully managed: in 2023, the market value of the plan’s investment portfolio was about $77 billion, with the plan delivering a 7.8% annualized return from 2013 to 2023.

DB vs. DC: what’s the difference?

You may have also heard about Defined Contribution (DC) plans, which are becoming more popular—especially in the private sector. In contrast to a DB plan, a DC plan does not promise a specific benefit amount at retirement. Instead, employees and/or employers contribute a set amount of money to an individual account within the plan. The amount available at retirement depends on what you put in and on how markets perform: employees carry all the risk.

In contrast, in a DB plan like the MPP, the risk is shared. The employer is responsible for ensuring a set retirement benefit, and your pension is not tied to the market ups and downs or changes in interest rates.

It’s true that employees can potentially accumulate more wealth in a DC plan. But it also comes with a lot more uncertainty, and certainly no guarantee of a specific income level in retirement.

With a DC plan, you’ll be responsible for managing the investment account, meaning you’ll need a good understanding of investing and market fluctuations. Additionally, DC plans offer no guarantee of sufficient funds at retirement. If an employee does not contribute enough during their working years or their investments perform poorly, they may face a shortfall in retirement or, at least, significant questions about the appropriate rate of decumulation of assets to enhance quality of life without literally “outliving” the assets. The consequences of a miscalculation in retirement can be serious.

Looking ahead

Ultimately, retirees rely on a variety of retirement vehicles in their golden years. Whether it’s defined benefits, defined contributions, or personal savings, the goal remains the same: to sustain a level of income that allows not only peace of mind but a preferred lifestyle in retirement. The earlier a person starts considering what this means for them, the better they can plan for the road ahead.

There’s more to explore about how the MPP works and we’ll be covering more about your retirement on HSA’s website.

But for now, take this to heart: a strong pension is a source of long-term security. It’s what will give you the ability to retire with dignity after a lifetime of providing others with care, support, and essential services. And it’s not something you have to manage on your own.

If you are interested in learning more about the MPP, the Municipal Pension Board of Trustees will host an annual general meeting on October 16 to report on the health of your pension plan.